The non-life insurance sector witnessed a decline in business during the first half of the fiscal year 2023/24 mainly due to a slowdown in economic activities.

BY NewBiz Team

Insurance companies were on a merging spree at this time in the last fiscal year. Every other day, a new merger agreement was being announced or a merger plan was being finalised. However, a year later, the non-life insurance sector is facing an entirely different scenario. Rather than the excitement of mergers, the sector is confronting challenges posed by an economic downturn and a slowdown in business activity.

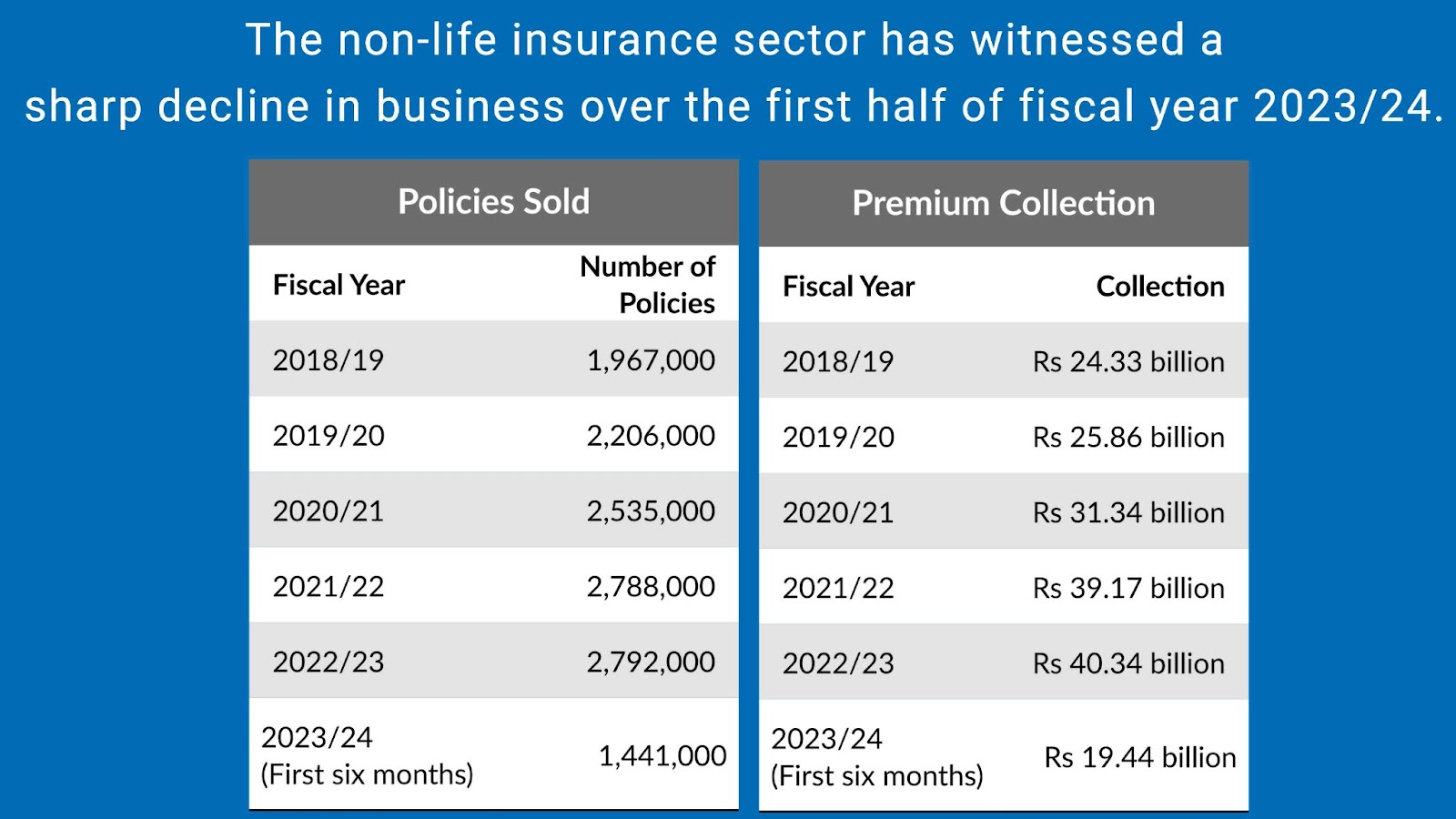

The non-life insurance sector has witnessed a sharp decline in business over the first half of fiscal year 2023/24. This stands in stark contrast to the scenario of just two years ago when the non-life insurance industry was enjoying a consistent double-digit growth. The sector experienced a remarkable 23.56% growth in business in fiscal year 2021/22.

The non-life insurance business had already started to feel the impact of the economic headwinds that faced the country in 2021/22. In 2022/23, the sector posted a modest growth of 2.66%. The total non-life insurance premium collection, which amounted to Rs 39.16 billion in 2021/22, rose to Rs 40.21 billion in 2022/23. However, the growth rate in premium collection turned negative in the first half of 2023/24.

Data compiled by the Nepal Insurance Authority (NIA) shows that the non-life insurance business shrunk by 3.19% percent in the first half of the current fiscal year. The insurance premium collection, which amounted to Rs 20.08 billion in the first six months of the previous fiscal year, decreased to Rs 19.44 billion in the review period.

Chunky Chhetry, CEO of Sagarmatha Lumbini Insurance Company, admits that the non-life insurance business has been affected by the recent economic slowdown.

The NIA data reveals a decline in various sectors of the general insurance business during the first six months of 2023/24. Engineering insurance experienced a significant drop of 22.30%, with non-life insurance companies recording Rs 2.81 billion in premium from the sector in the review period, compared to Rs 3.61 billion in the same period of 2022/23. This decline is attributed to reduced construction activities in the country.

Likewise, agricultural insurance witnessed a 12% decline in premium collection to Rs 960 million in the review period compared to Rs 1.09 billion in the corresponding period of the previous fiscal year. Motor insurance - the largest sector in terms of premium collection - saw a decline of 3.49% during the period. Non-life insurance companies generated a business of Rs 6.22 billion from the sector during the first six months of 2023/24, compared to Rs 6.55 billion in the same period of the previous fiscal year.

Property, aviation and miscellaneous sectors witnessed growths of 6.14%, 8.28% and 7%, respectively, while the micro-insurance business posted an impressive growth of 50% compared to the first six months of the previous fiscal year.

In terms of policies sold, however, there was a decrease of 15.46% in engineering insurance, 14.47% in agricultural insurance, 3% in motor insurance, 13.63% in aviation insurance, and 5.22% in miscellaneous insurance.

According to the NIA, non-life insurance companies sold 1.44 million policies in the first half of the current fiscal year, only slightly higher than 1.39 million policies sold during the same period last fiscal year. Although there has been a nominal uptick in the number of policies sold, data shows large-sum insurance transactions have come down. As a result, premium collection has dropped despite the rise in the number of policies. Non-life insurance companies attribute this decline to a reduced insurance activity in sectors such as automobile and construction which typically involve substantial policy amounts.

Slump in economic activities

The Nepali economy faced a multitude of challenges in the post-COVID scenario. This was compounded by the emergence of the Russia-Ukraine conflict, liquidity crises, surging interest rates, and import control measures amid diminishing demand. As a result, the Nepali economy expanded at a slower rate of 1.9% in 2022/23.

Traditional insurance products continue to dominate the non-life insurance business in Nepal as companies have not been able to bring new and innovative products.

A discernible slowdown has been evident across key sectors like construction, industry, services, banking and the capital market. This has had a ripple effect on the insurance industry. Although the sector showed great resilience during the pandemic, the non-life insurance industry has now succumbed to the broader economic downturn, experiencing a decline following years of robust growth.

The non-life insurance sector is deeply intertwined with economic activities. A majority of its business is heavily dependent on industrial operations, construction activities, import-export dynamics and the automobile industry. "Unfortunately, the recent economic slowdown in Nepal has significantly impacted non-life business operations," Chhetry of Sagarmatha Lumbini Insurance Company told New Business Age.

Automobile insurance used to contribute the largest share in the business of non-life insurance companies in the past. However, the automobile sector has witnessed a decline in Nepal over the past two years in response to dwindling foreign exchange reserves, and the import restrictions on various items including high-end vehicles for nine months. Although these restrictions were lifted in December 2022, the demand for motor vehicles has not recovered. Non-life insurance companies say that the downturn in the automobile industry has directly impacted their business.

Motor vehicle insurance is compulsory in Nepal. When there is a surge in motor vehicle transactions, the insurance sector experiences a corresponding increase. With automobile sales on the decline, the insurance industry is feeling the heat. Similarly, due to a reduced market demand, numerous industries have downsized their production. As a result, the insurance cover these companies buy for storing goods has also decreased. This downturn in business activity has resulted in a decrease in other types of insurance as well.

Neco Insurance CEO Ashok Khadka says there is a direct correlation between bank loans and the insurance industry. "Growth in credit disbursement typically parallels growth in insurance. With current low loan disbursement rates, the insurance sector cannot sustain its growth trajectory," said Khadka.

12 non-life insurance companies merged to form six entities. This resulted in a reduction of the number of non-life insurance companies to 14 from 20.

The deceleration in the construction industry has also impacted the non-life insurance sector. Engineering insurance is crucial during the construction of vital infrastructure like hydropower projects, roads, bridges and commercial buildings. However, the construction sector has faced numerous hurdles in recent years, primarily stemming from the skyrocketing prices of construction materials, delays in government payments to contractors, and temporary shutdowns in the crusher industry. Contractors lament that they are still awaiting government payments amounting to Rs 10 billion for works already completed. Furthermore, the slowdown in foreign trade has adversely affected shipping insurance.

"Investments in public infrastructure projects are not increasing. The insurance sector is remaining stagnant in the absence of economic activity in the country," CEO Chhetry said. "Until there's a resurgence in economic momentum, the insurance business will struggle to gain traction." According to Chhetry, only property insurance is witnessing satisfactory business at the moment.

Neco Insurance CEO Khadka said that insurance is inherently reliant on compulsion. "Unless made mandatory, the insurance sector struggles to thrive. Presently, there are compulsory provisions for automobile insurance and obtaining bank loans. These mandatory requirements have facilitated the growth of non-life insurance companies. However, automobile sales have been lackluster lately, further affecting insurance uptake," said Khadka.

Moving ahead

Insurance experts say that non-life insurance companies must navigate the current challenges by exploring innovative solutions to boost their business. Traditional insurance products continue to dominate the non-life insurance business in Nepal as companies have not been able to bring new and innovative products. CEOs of insurance companies also acknowledge the necessity to venture into new domains and introduce innovative products to expand their business.

Sunil Ballav Pant, CEO of NLG Insurance, said the dependence on old-fashioned and conventional insurance products is becoming a challenge for business expansion. “It has been a year since non-life insurance companies encountered this problem. We won’t make any progress if we continue with the current approach,” Pant said. “Insurance companies must introduce new products to expand their business. There is a great opportunity in the health sector as we still lack insurance products that cater to this sector.”

Non-life insurance companies say they need to bring new products specifically tailored for agriculture and livestock insurance. Since most of the farming and animal husbandry activities remain uncovered by insurance, companies that bring innovative products can expand their business significantly.

Companies also called on the government to bring policies aimed at stimulating economic activity, increasing capital expenditure, and ensuring timely payments to construction companies. Additionally, they urged the government to implement policies to provide insurance coverage for physical infrastructures. Experts also say that local governments should establish policies to ensure the physical property and health of their residents. Furthermore, they also called on the government to enhance public awareness regarding non-life insurance to foster greater understanding and participation in these vital financial protections.

Call to tap new areas

Companies say they have realised the necessity to diversify their investments into new areas. Currently, many companies are opting to keep funds in bank term deposits and interest is a primary income source for many companies. However, the volatility of interest rates in the open market directly impacts the income of insurance companies. Moreover, with declining interest rates and the inherent instability of the stock market, experts called on the companies to broaden their investment portfolios instead of relying on their traditional business.

Pant, the CEO of NLG, said companies must expand investments into new sectors. Stating that the regulatory body has already laid down a legal framework for insurance companies to invest in sectors such as real estate, hydropower, agriculture, and tourism, Pant said insurance companies need to invest in these areas to capitalise on emerging opportunities and diversify the investment portfolio. “Current business and market conditions require insurance companies to expand investments into new sectors. Nevertheless, it's crucial to maintain a long-term perspective and focus on areas offering reasonable returns rather than seeking immediate results," he added.

Chhetry, CEO of Sagarmatha Lumbini Insurance, said the insurance sector should increase investments in infrastructure projects. To ensure secure investments, he even proposed that the government introduce insurance bonds. "Since we are in the risk-bearing business, reckless investments can jeopardise our ability to fulfil insurance claims in the future. Therefore, it's imperative to make prudent and safe investment decisions," he added. “In this context, I believe the government should consider issuing insurance bonds with a reasonable interest rate. This will not only ensure the safety of investments for insurance companies but also guarantee reasonable returns. Additionally, it would help the government in capital mobilisation."

The government did announce plans to issue insurance bonds in the previous budget. However, it hasn’t materialised. Although insurance companies have been investing in various government bonds, they argue that this alone is insufficient to meet their investment needs.

Mergers failed to generate anticipated synergies

In the previous fiscal year, the NIA introduced a new capital floor for insurance companies which triggered a merger and acquisition spree in the industry. Consequently, 12 non-life insurance companies merged to form six entities. This resulted in a reduction of the number of non-life insurance companies to 14 from 20.

The NIA raised the paid-up capital requirement for both life insurance and non-life insurance companies, from Rs 2 billion to Rs 5 billion and from Rs 1 billion to Rs 2.5 billion, respectively. While many companies met these requirements through mergers, others employed strategies such as rights issues, asset sales, and partnerships.

Despite the NIA's efforts to promote mergers, CEOs of insurance companies expressed dissatisfaction, stating that the consolidation has failed to yield the desired outcomes.

Chhetry lamented that his company could not fully capitalise on the benefits of the merger due to financial constraints. "We were expected to see the benefits of the merger this year. However, due to economic slowdown, the synergies of the merger have not materialised yet," he stated. "If this trend continues, it may take at least two more years to realise the full impact of the merger.”

Rajuraman Paudel, the executive director of the NIA, echoed similar sentiments. "The state of economic activities directly affects the insurance sector. While insurance companies have indeed strengthened post-merger, the anticipated benefits have not been seen due to the economic slowdown," he explained.

Surge in profits

Despite a contraction in business, the profits of non-life insurance companies have increased. In the first six months of the current fiscal year, the net profit of the non-life insurance companies has increased by 42.65% to Rs 3.85 billion in the first half of 2023/24 compared to Rs 2.10 billion during the same period of 2022/23.

The profit of non-life insurance companies increased by 44.69% in the previous fiscal year to Rs 5.17 billion profits, compared to Rs 3.57 billion in 2021/22. Insurers say their profits improved mainly due to the high interest rates on deposits of banks and financial institutions. Insurance companies keep most of their investable capital in fixed deposits of commercial banks.

We've been Impacted by the Economic Downturn

• The economy continues to show signs of weakness as investment in development construction remains stagnant. Investments in public infrastructure projects are not increasing. The insurance sector remains stagnant in the absence of economic activity in the country.

• As economic activity remains subdued, motor vehicle sales have failed to meet expectations. Currently, property insurance is the only segment showing satisfactory performance. Until there's a resurgence in economic momentum, the insurance business will struggle to gain traction.

• The anticipated synergy from recent mergers in the insurance sector has yet to materialise, primarily due to the ongoing economic recession. It appears that we may need to wait two more years for this synergy to manifest.

• The insurance sector should increase investments in infrastructure projects. To ensure secure investments, the government should introduce insurance bonds. I believe the government should consider issuing insurance bonds with a reasonable interest rate. This will not only ensure the safety of investments for insurance companies but also guarantee reasonable returns. Additionally, it would help the government in capital mobilisation.

We need New Products to Expand our Business

• We cannot address the current challenges by sticking to traditional products alone. Continued reliance on old-fashioned insurance products can hinder our business growth. Insurance companies, therefore, must innovate and introduce new products to expand their market.

• Current business and market conditions require insurance companies to expand investments into new sectors. Nevertheless, it's crucial to maintain a long-term perspective and focus on areas offering reasonable returns rather than seeking immediate results

• Prioritising health insurance is essential, as the current offerings in the sector may not adequately meet customer needs. There is a significant untapped potential in this area.

Introducing New Insurance Products may not Bolster Business

• Currently, industries in Nepal are operating at only 30-40% of their capacity. Import levels have decreased due to low domestic demand and consumption. Banks are facing challenges in lending as demand for loans remains subdued. Consequently, the economy is in a sluggish state, impacting the non-life insurance sector as well.

• The correlation between bank loans and the insurance industry is direct. Growth in credit disbursement typically parallels growth in insurance. With current low loan disbursement rates, the insurance sector cannot sustain its growth trajectory.

• In the existing climate, introducing new insurance products may not bolster business. If customers lack interest in existing insurance schemes, the introduction of new products is unlikely to succeed.

• Direct measures specifically targeting the insurance sector may not be necessary. Instead, increasing public expenditure and ensuring timely payments to contractors can have a positive trickle-down effect on the insurance industry.